The end of venture subsidised AI

Venture capital funded AI adoption at artificially low costs. Now compute is getting more expensive and capital is tightening. My take on what happens when the subsidy ends and unit economics actually matter.

6 min read

Venture capital funded a particular kind of AI adoption. Not because the economics made sense yet, but because the narrative did. At least that is how it looked from the outside. Investors seemed willing to pay for scale, for logos, for the optionality that maybe this AI thing would solve a real problem eventually. Startups adopted accordingly.

The equation appeared straightforward. Use compute aggressively. Build features that looked good in demos. Investors would fund the burn. Unit economics could wait. This worked for a while because the cost of inference stayed relatively low and the availability of capital stayed relatively strong.

Both of those things seem to be changing at the same time.

The pricing shift is real, but what it means is unclear

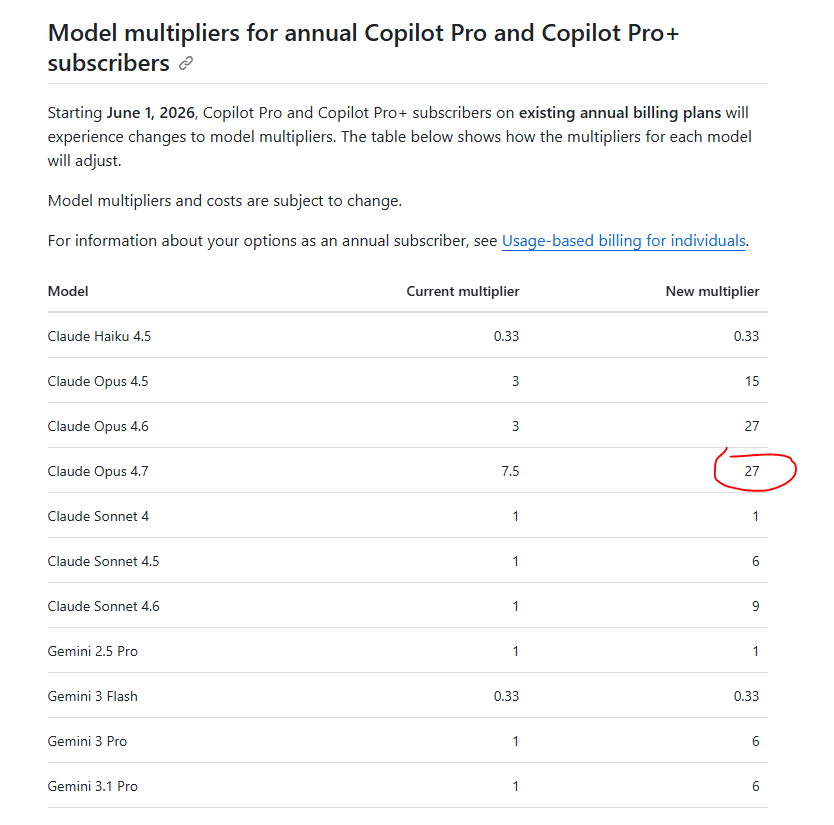

On June 1, 2026, Anthropic is moving Claude Opus 4.7 from a 7.5x multiplier to a 27x multiplier for annual Pro and Pro+ subscribers. I am not sure if this is a surprise anymore. It was signalled. But it is also probably not an outlier. The cost of using frontier models appears to be going up. Compute is getting more expensive because better models cost more to run. Whether the era of dirt cheap inference is genuinely over is harder to say.

At the same time, I have noticed venture funding for AI startups seems to have tightened. The number of seed rounds funding “we built AI on top of X” has dropped noticeably in my reading of announcements and discussions. The capital that was underwriting cheap compute usage might be drying up, or it might just be moving elsewhere. Founders seem to be getting asked harder questions about what their product actually does and whether anyone would pay for it at real prices.

When unit economics actually matter

What I suspect will happen next is a shift in how startups think about AI. Not whether to use it, but where it might actually create value. This is not new thinking for most software businesses. It is probably new thinking for the AI companies that grew up in what felt like a venture subsidy era.

The ones that seem most likely to weather this are the ones that can answer a specific question: does this AI feature create enough value that customers would pay for it at cost plus margin? Not at some theoretical cost when inference is cheap. At actual costs right now.

This question forces you to be specific. An AI feature that saves ten hours of manual work per month is probably not valuable if your customer is paying $5,000 a month to run it. An AI feature that automates a $200,000 per year process might be valuable even if it costs $40,000 a year to run. But I could be wrong about the thresholds.

The math is straightforward enough. But it requires founders and product teams to do something they have been able to avoid for a while. Actually understand the unit economics of their AI features.

What this actually means

This is not necessarily a bad thing. My instinct is that most of those products probably should not have been built in the first place. The venture subsidy made it possible to build things that created no obvious value and still raise money. Whether that era is actually ending is the real question.

What strikes me about this moment is that it is not actually an AI problem. It is a return to normal software business logic. Build something people will pay for. Make sure you understand your costs. Price it so you make money. This is how every other software company has always worked. It might be how AI companies are going to have to work now, or it might not be.

The companies that seem best positioned are the ones that spent the last few years thinking about this already. The ones that are probably going to struggle are the ones that treated venture funding as a substitute for business model clarity.

The math is the problem, not the pricing

If you have not done the math on your AI features, it might be worth starting now. Figure out what they actually cost. Figure out what they are actually worth to your customers. If there is no clear way to make those two numbers work, you probably have a bigger problem than model pricing.

The shift on June 1 is not the cause of that problem. But it might be the moment when it becomes harder to ignore.

By Curtis Blunden

1 May 2026